[CHECK AGAINST DELIVERY]

[Introduction]

It is not hard to spot that we are living in disruptive times, for good or for bad. This means that crisis readiness is as important, perhaps more so, than ever. Those same developments also put a premium on effectiveness and clarity in how we deliver on this operational readiness. I would like to share with you how we approach this at the Single Resolution Mechanism and discuss why crisis readiness goes well beyond banks and resolution authorities.

ISDA has been part of finding practical solutions to ensuring effective market procedures for a long time. It is the perfect fora to talk about ensuring that the evolving financial system is not only resilient but also resolvable by design.

1. Practical crisis readiness

At the Single Resolution Board, as you may know, we are responsible for banks headquartered in the banking union and work closely with other resolution authorities worldwide as the largest banks in the world typically have a presence in the EU.

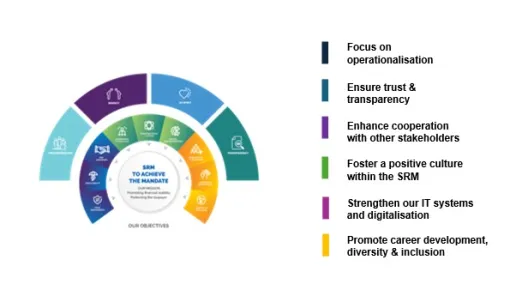

After years of developing plans and building up capacities and expectations, our focus now is on operationalisation. As set out in our vision and work programme for this year, this will include:

* Explaining resolvability expectations more clearly and concretely

* A multi-year programme of bank-led testing

* The SRM approach to simplification.

Single Resolution Mechanism: Vision 2028 strategic objectives[1]

Those elements are reinforcing: simpler processes and reporting set ups give us and banks more time to focus on what matters. Simulation exercises shine light on where more is needed and where processes are already robust. Predictability in planning and stability in guidance and expectations underpin this. Stabilising the framework, focussing on ‘good enough’ and giving clarity on the way forward reduces compliance cost and complexity for everyone.

SRB Working Priorities 2026[1]

Let me illustrate that by one of our 2026 priorities: testing. Banks test their crisis readiness following a multi-annual testing programme, giving them and us assurance of their ability to execute.

That means: to ensure that governance processes and mechanisms are in place, that the banks’ management information systems operate effectively in a resolution scenario, and that the actions set out in procedural manuals or ‘playbooks’ produce the expected results.

The operational effectiveness of resolvability capabilities should be engrained in a bank’s overall risk management. It is important that banks include crisis preparedness in their business-as-usual work and have the appropriate governance around it.

So far, I spoke mostly about what we are doing and what we are requesting of banks. But resolvability readiness is not only about resolution authorities or banks. A successful resolution can require understanding and action by counterparties as well. It is important that market players are well informed and sufficiently engaged on resolution matters. This increases the understanding of the technicalities and the implications of resolution work for a stable financial system - which is so crucial for the market reaction to resolution action. This is why we appreciate the work by ISDA in analysing, for example, how termination, close-out rights and remedies may be affected by the application of stays and creditor safeguards in resolution.

2. Focused crisis preparation

Let me now turn to substance. While we know that every crisis is different, it is equally clear that we can and have to prioritise and offer predictability. That means exercising judgement on the degree of the operationalisation of tools, resolvability assessments, and testing activities for each bank. It does not mean taking a narrow view or compromising on our mandate.

This is why we have set out clear “expectation for banks”, alongside more practical operational guidance, why we develop multi year programmes embedded in our vision and why we pursue simplification efforts in our own processes and in supporting others.

This clarity on priorities and focus does, however, not mean assuming that there is one single solution. We must adapt resolution tools and strategies to what best serves specific circumstances. As we saw play out in recent crisis cases, it was important to be able to adapt and combine resolution tools and have alternative strategies available.

Another focus of crisis readiness includes readiness for a hybrid crisis where financial risks interact with non-financial risks such as cyberattacks, sanctions or third-party provider issues.

We need to think about the toolkit and the approach to coordination for those complex situations, both in dealing with entities and in protecting critical functions. The current resolution toolkit does not offer easy solutions.

For example, while the resolution framework in itself is not designed or mandated to fix ICT incidents, these are becoming a potential source of increasing disruption in the financial sector. The European Digital Operational Resilience Act – DORA -, which came into force last year, will raise standards in terms of resilience to ICT disruption. In addition, under DORA the SRB receives reports from banks that encounter major ICT incidents, and participates in the new EU systemic cyber incident coordination network, and all this increased information sharing is a helpful step in the right direction.

3. Forward looking planning for crisis

It is generally easier to build in crisis readiness than to retrofit it. We should aim for structures that are resolvable by default and by design.

In this context, let me highlight three developments:

New technologies are leading to near instantaneous market responses and transactions. This can increase the speed and intensity of a developing crisis and challenge a timely and effective crisis response.

We should consider what will act as effective firebreaks to this transmission, should it be needed.

One aspect of this time sensitivity can be addressed by statutory and contractual stays as part of bank resolution regimes. Again, the ISDA Resolution Stay Jurisdictional Modular Protocol and ISDA’s analysis in the context of its close-out framework have contributed to the awareness of these options.

Innovations in wholesale markets are changing financial transactions.

For example, how do stablecoins affect crisis preparation? What impact on banks’ resolvability do we expect from stablecoin settlement services, issuance or automated systems?

Where the issuer of a token is a bank, the SRB will consider this in its resolution planning. For instance, MiCAR stipulates the right of investors to redeem their tokens at any time, and the SRB will assess, upon the notice from the competent authority, the redemption plan and consider if any actions in such plan might adversely impact the resolvability of the issuer and thus could require any changes to the resolution plan or the resolvability of the bank.

A trend of greater interaction between banks and non-banks – and more broadly, a greater modularisation of finance – changes the landscape of counterparties in the banking system.

Where key functions are dispersed widely, potentially with low substitutability, the loss of one function in a failure event could affect others in new ways. As the system develops, making sure that functions and institutions are resilient and resolvable by design will help future crisis readiness.

Conclusion

Practical, focussed and forward-looking work on crisis readiness involving all counterparties will help us to ensure that, when the next crisis comes, we are prepared to deal with it. Thank you for the opportunity to engage with you on these topics today.

[1] SRB Work Programme 2026: https://www.srb.europa.eu/system/files/media/document/2025-11-26_SRB-Work-Programme-2026.pdf

Contact our communications team

Recent news

Related news and press releases