Raising of the contributions

The contributions raised from the banks to the SRF are known as ex-ante contributions or extraordinary ex-post contributions. Almost all banks, big and small, across the Banking Union, must pay those contributions.

The SRB is responsible for the calculation of these contributions. The way the SRB calculates how much each institution owes is set out in Regulation (EU) No 806/2014, Commission Delegated Regulation (EU) 2015/63 and the Council Implementing Regulation (EU) No 2015/81. This is to ensure fairness when deciding how much each bank owes.

As part of the calculations methodology, the SRB has developed uniform data definitions, a data reporting form and guidelines for all institutions.

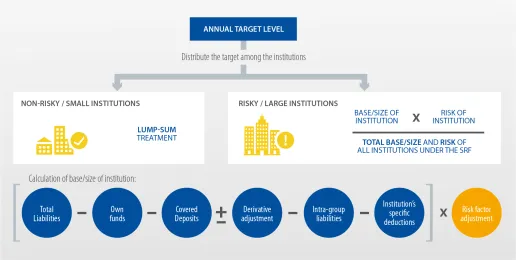

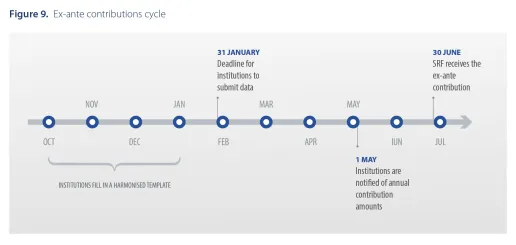

In order to allow the SRB to calculate the individual contribution, institutions are required to report data to the SRB. Institutions therefore need to report data to the NRAs by 31 January of every year at the latest. Where an institution does not submit all the required data on time, the SRB may use estimates or its own assumptions in order to calculate the annual contribution of the institution. In certain cases, the SRB may assign the institution concerned to the highest risk adjusting multiplier. The calculation of individual ex-ante contributions largely derives from the target level of at least 1% of covered deposits and from the size and the risk of each individual institution.

The NRAs are responsible for the collection of the ex-ante contributions and then they transfer them to the SRF no later than 30 June each year.

Where the available financial means of the SRF are not sufficient to cover the losses, costs or other expenses incurred by the use of the SRF in resolution actions, extraordinary ex-post contributions may be raised in addition.

Mutualisation of the contributions

During the eight year initial period, contributions raised by NRAs at national level and transferred to the SRF were allocated to national compartments corresponding to each of the 21 Banking Union countries.

All national compartments have been merged and ceased to exist at the end of the eight year initial period. The available financial means in the SRF are now fully mutualised.